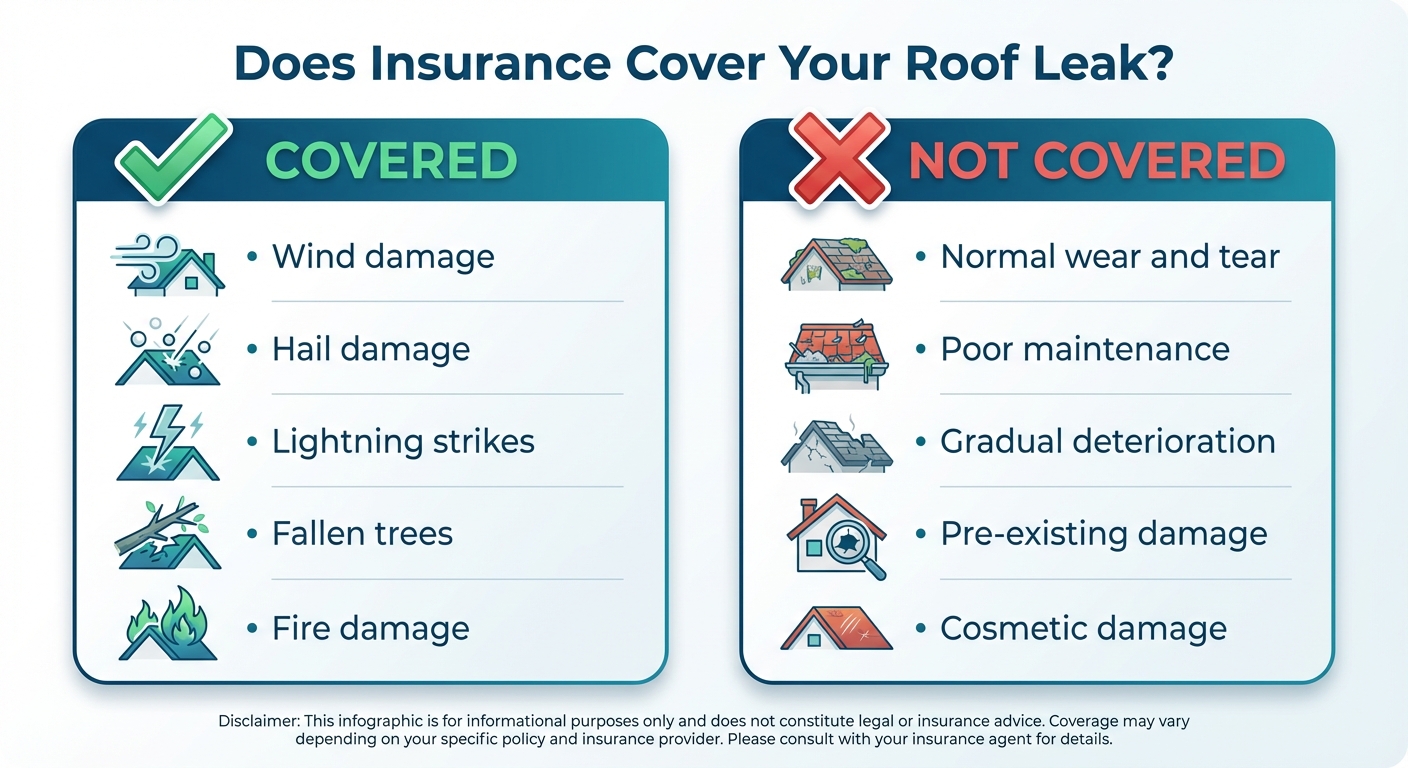

Yes, homeowners insurance typically covers roof leak repairs in Thonotosassa, FL — but only when the leak is caused by a sudden, accidental event such as storm damage, fallen trees, or hail. Standard Florida homeowners policies (HO-3) cover the cost of repairing or replacing a roof damaged by covered perils including wind, lightning, fire, and falling objects. However, insurance will not pay for leaks caused by normal wear and tear, lack of maintenance, or gradual deterioration over time.

In Thonotosassa and Hillsborough County, hurricane and tropical storm damage claims are the most common roof insurance claims. Your out-of-pocket cost depends on your deductible — Florida policies typically have a separate hurricane/wind deductible of 2%–5% of your home's insured value. Thonotosassa AquaBarrier Roof Solutions works directly with insurance adjusters and can provide the documentation your claim requires, including detailed inspection reports and repair estimates.

Key Takeaways

- Insurance covers roof leaks from sudden events (storms, hail, fallen trees) — not wear and tear

- Florida HO-3 policies cover wind, lightning, fire, and falling object damage

- Hurricane deductibles in FL are typically 2%–5% of insured home value

- Proper documentation from a licensed roofer strengthens your claim

- Filing promptly after damage is critical — delayed claims get denied more often

Roof Leak Insurance Coverage in Thonotosassa, FL

What Roof Leak Damage Does Insurance Cover?

Florida homeowners insurance policies cover roof damage caused by covered perils — specific events named in your policy. The most common covered perils for roof leaks in Thonotosassa include:

- Wind damage: Missing shingles, lifted flashing, or exposed decking from storms or hurricanes

- Hail damage: Cracked, bruised, or punctured shingles from hailstones

- Fallen trees or branches: Impact damage from trees brought down by storms or natural causes

- Lightning strikes: Direct strikes that crack, burn, or structurally damage roofing

- Fire damage: Any roof damage resulting from fire, including neighbor fires

The key distinction is sudden vs. gradual. If a storm rips shingles off your roof tonight and rain comes in tomorrow, that is a covered event. If your 20-year-old shingles have been slowly deteriorating and finally start leaking, that is maintenance — and insurance will not cover it. Insurers look at the proximate cause of the damage. If an adjuster determines the leak existed before the storm, or that the storm merely exposed pre-existing deterioration, the claim may be partially or fully denied.

Insurance also typically covers resulting interior damage — water-stained ceilings, damaged drywall, ruined insulation — as long as the roof damage itself was caused by a covered event. This is important because interior water damage can sometimes cost more to repair than the roof itself.

Understanding Florida Hurricane Deductibles

Florida is one of the few states with a separate hurricane deductible that is significantly higher than your standard deductible. While your regular deductible might be $1,000 or $2,500, your hurricane deductible is calculated as a percentage of your home's insured dwelling value — typically 2% to 5%.

Here is what that looks like for a typical Thonotosassa home:

- $250,000 home with 2% hurricane deductible: $5,000 out of pocket before insurance pays

- $300,000 home with 2% hurricane deductible: $6,000 out of pocket

- $300,000 home with 5% hurricane deductible: $15,000 out of pocket

- $400,000 home with 2% hurricane deductible: $8,000 out of pocket

The hurricane deductible applies only when a hurricane or tropical storm triggers the damage. For non-hurricane wind damage, hail, fallen trees, or lightning, your standard (lower) deductible applies. The distinction matters: if a routine thunderstorm — not a named tropical system — damages your roof, you pay your regular deductible, which could save you thousands. Make sure you know which deductible applies before filing.

How to File a Roof Leak Insurance Claim in Thonotosassa

Filing a roof damage claim the right way increases your chances of full approval. Follow these steps:

- 1. Document immediately: Take photos and video of all visible damage — roof, ceilings, walls, attic — as soon as it is safe to do so. Timestamp everything.

- 2. Prevent further damage: Place tarps or buckets to stop ongoing water entry. Insurance expects you to mitigate further damage, and emergency tarping costs are typically reimbursable under your policy.

- 3. Contact your insurance company: File the claim promptly. Florida law requires insurers to acknowledge your claim within 14 days and make a coverage decision within 90 days, but earlier filing gives you a stronger position.

- 4. Get an independent inspection: Before or alongside the adjuster's visit, have a licensed roofer inspect the damage and provide a detailed written estimate. This gives you leverage if the adjuster's estimate comes in low.

- 5. Meet with the adjuster: Be present when the insurance adjuster inspects your roof. Having your roofer there at the same time ensures nothing is overlooked.

- 6. Review the estimate carefully: Compare the adjuster's estimate to your roofer's estimate. If there is a significant gap, you have the right to negotiate or request a re-inspection.

At Thonotosassa AquaBarrier Roof Solutions, our team handles the inspection and documentation process for you. We provide detailed photo reports, damage measurements, and line-item repair estimates formatted for insurance submission — at no cost to you.

When Insurance Will Not Cover Your Roof Leak

Understanding what is not covered helps you avoid filing a claim that will be denied (which can negatively impact your claims history). Insurance typically will not pay for:

- Normal wear and tear: Shingles that have degraded naturally over 15–25 years

- Deferred maintenance: Leaks around areas that should have been maintained (clogged gutters causing backup, unsealed penetrations)

- Roofs past expected lifespan: Many Florida insurers will not fully cover roofs older than 20 years, or may only pay actual cash value (depreciated) rather than replacement cost

- Cosmetic damage only: Hail dents that do not affect function may not meet the claim threshold

- Pre-existing damage: Damage that existed before your policy started or before a reported event

Even when insurance does not cover the leak, repairs are still affordable. Most Thonotosassa roof leak repairs cost $350–$1,500 out of pocket. And if your roof needs more work than expected, understanding the 25% roof rule will help you plan whether a repair or replacement makes more financial sense.